These are turbulent times, arguably the most uncertain since at least the Great Recession. At M3, however, we’re always focused on investing with a long-term outlook. We consider ourselves the gatekeepers of your wealth, and we want to ensure you can preserve your and your family’s financial future, especially when uncertainty abounds.

Given the current situation, as the Federal government and the States begin to organize and coordinate phase two of the Coronavirus response, we think it is important to talk about what lessons we can draw from this unprecedented lockdown, to ensure that your long-term goals and your life’s work are both always safeguarded.

Let’s dive right in.

What can we learn from COVID 19?

It is too soon and too insensitive to write a blog post on what the government response was or should have been, and it is not my place to do so. Some point to misleading information from China about the virus, and warnings in the US about preparing for the next pandemic that the government ignored, or the alleged lack of preparation for a crisis, ahead of today’s needs or political priorities. This certainly is not the time to recriminate, especially as so many are struggling through this crisis. This is the time to stand together and focus on how to handle the crisis at hand.

There will be a moment of reckoning, in which we will have to look at what lessons the government can learn from this Global Pandemic, we can consider how this will impact our relationship with China, future trade negotiations and changes in the US supply chain of essential items, however, individuals already can learn something about personal finances from this situation.

The truth is that many households are already feeling the financial impact of the crisis. It is our belief that financial planning and discipline can make the difference in how to survive it.

Americans’ Personal Finances

Many Americans live paycheck to paycheck. According to a 2017 survey by CareerBuilder, a leading jobs site, as many as 78% of U.S. workers live paycheck to paycheck to make ends meet. And this is not limited to lower earners: Nearly one in 10 workers making more than $100,000 a year also live paycheck to paycheck and more than 1 in 4 workers do not set aside any savings each month.

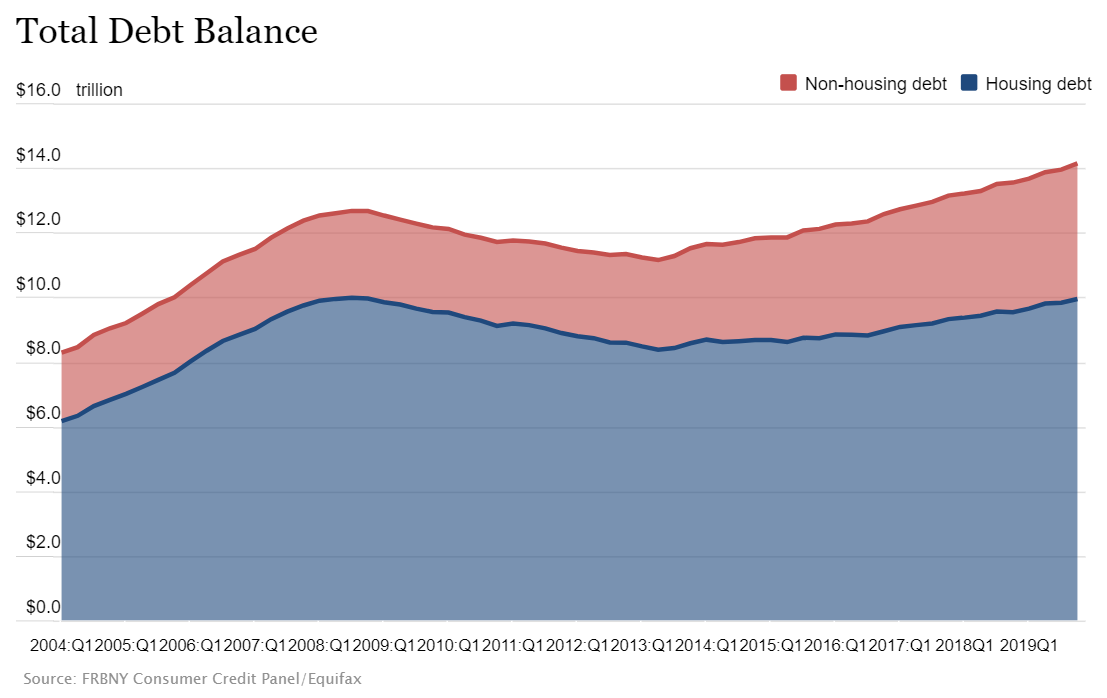

Further, although housing debt is still slightly below the level reached in 2008, non-housing debt has surpassed its previous peak, standing at $4.2 trillion at the end of 2019, as the New York Fed reports.

As the unemployment rate ticked up to 4.4% in March, after about 22 million Americans filed for unemployment benefits over the past four weeks, many think unemployment may even be approaching Great Depression levels at 18%, as reported by Fortune.com.

When living paycheck to paycheck and suddenly losing your job, the situation gets tough fast. All of this is happening while the IRS raised a warning of the possibility of debt collectors garnishing the stimulus check that has begun being disbursed.

The M3 philosophy is that one must take control and plan out the future. You won’t avoid all financial pain in a crisis, but you will be in a better position and better prepared when one comes.

Core financial beliefs of M3

Even if it’s not glamorous, we’ll say it right away: you have to live below your means. But what does that mean? In his budgeting and investment guide, Straight Talk on Investing, Jack Brennan, former CEO of Vanguard, sums up like this: “living below your means” is focusing on saving any nonessential income you may have rather than making impulse purchases. Save first, spend later!

This implies that determining your financial goals and devising a plan to steadily address them within a predetermined budget comes first. Then, non-essential spending follows. In order to do so, you must know the difference between needs and wants. There is a battle raging in everyone’s wallet, and it’s won with discipline and planning.

This might seem obvious to some, but you have to spend less than what you earn. Save first, have a budget and live on what is leftover, and when you get a raise, increase your savings as well, not just spending. Stay away from debt if possible, pay off every credit card every month, and if you cannot afford to do that, then you cannot afford what you bought.

Save, save and then save! And have an emergency fund – one month, maybe two (ideally six) of cash flow. If you cannot do this, cut your expenses and adjust your lifestyle. If you do not, you are building your financial life in shifting sands.

Invest based on your risk tolerance and the duration of when you need the money. Warren Buffet has said that if you are not prepared to lose 40% to 50% of your money, then don’t invest in stocks! Always think ahead.

The Bucket Approach

Take a bucket approach to all your portfolio based on when you will need to take money out. The first bucket is money you’ll need in the next 5 years, the second in the following 5, and so on until you have confidently planned for 25 years ahead.

Let’s take the current situation for instance: having cash holdings in the first bucket (0-5 years) buffers savers psychologically from the market decline. This way, the investor can avoid taking withdrawals from stocks while the market is down. Thus, when the stock market performs poorly, money can be taken out from the cash account, and when the stock market does well, investments can be also sold to replenish cash. Bucket strategies provide peace of mind and help clients stay with their long-term plans.

It really does not matter much what you are saving for. Saving for a car, for a down payment on a house, for college or for retirement, always consider the time period of when you will need the money. This will allow you the foresight and the tranquility of not having to take the money out when the markets are collapsing. An investing maxim is “buy low and sell high”, but that implies planning around being forced to sell low because you need the money at that moment! The money you need for the next 5 years should be safe, and this way you won’t get caught in the panic of selling at the bottom because you are scared and need it right away.

Conclusion

These are difficult times for everyone. But as people, we cannot prepare for Pandemic scenarios unless we can afford to build bunkers and live with an apocalypse-watch mentality. What we can do instead, is live within our means and save for our financial future. This will allow us to be prepared and less vulnerable if any unexpected circumstances come about.

At M3, we put our philosophy into practice to make sure we are the gatekeepers of your wealth while working to safeguard your financial future. If you are concerned about your plan and cash flow, our M3 Command center is a powerful tool that can provide you with the confidence to know your baseline and future.